Ibbotson Asset Allocation

Table of Contents Heading

- Jumping Over A Low Hurdle: Personal Pension Fund Performance

- Asset Allocation Calculator

- Lifetime Financial Advice: Human Capital, Asset Allocation, And Insurance

- Our Managed Portfolios

- Hot Issues Market

- Lessons From 5 Decades Of Asset Allocation

- Thoughts On roger G Ibbotson: What Works In Asset Allocation

It examines the factors which can potentially affect the real return of pension portfolios in different countries. The authors study the impact of more liberal investment limits on the composition and structure of pension investment portfolio, as well as anti-inflationary policy, on raising the real return. They also examine the factors which predict the degree of severity of asset allocation requirements for pension portfolios in different countries, and estimate the likelihood of their relaxing for Russian pension funds and managing companies. The aim of diversification is to avoid each extreme, allowing investors to achieve high returns while reducing volatility along the way and making it unlikely that they will suffer from a permanent loss of capital.

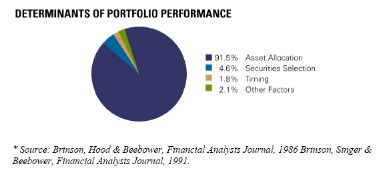

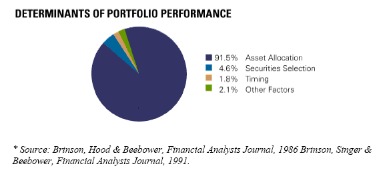

Drawing a parallel for equity-only portfolios, this study analyzed the importance of allocation by economic sector and by size and style in purely U.S. stock portfolios and the importance of regional allocation policy in international stock portfolios. The study found that allocation policy explains one-third to nearly three-quarters of among-fund variation in returns, nearly 90 percent of across-time variation, and more than 100 percent of the level of stock portfolio returns. Disagreement over the importance of asset allocation policy stems from asking different questions, We used balanced mutual fund and pension fund data to answer the three relevant questions. This article discusses the impact on performance of the long-term asset allocation policy relative to the impact of active management. Most of the variation in time-series returns for a typical fund comes from general market movement.

Jumping Over A Low Hurdle: Personal Pension Fund Performance

Ibbotson’s well-respected EnCorr software package for investment management and strategic asset allocation complements many of Morningstar’s research and portfolio tools for institutions and advisors. Ibbotson’s database of long-term capital markets returns will enhance Morningstar’s comprehensive security-specific data. Ibbotson also provides asset allocation, forecasting, and optimization software that is embedded in broker-dealer advisor platforms; this software complements Morningstar’s Web-based Advisor Workstation software. An asset-allocation fund or a balanced fund is a mutual fund that holds multiple asset classes . Typically these funds hold a stock component; a bond component, and in some instances, a cash component.

Core-satellite allocation strategies generally contain a ‘core’ strategic element making up the most significant portion of the portfolio, while applying a dynamic or tactical ‘satellite’ strategy that makes up a smaller part of the portfolio. In this way, core-satellite allocation strategies are a hybrid of the strategic and dynamic/tactical allocation strategies mentioned above. Although the risk is reduced as long as correlations are not perfect, it is typically forecast based on statistical relationships that existed over some past period. Studies of these forecasting methods constitute an important direction of academic research. Along with globalization, new technologies are introduced to the banking sector in order to enhance service quality which is consequential to attract and retain rational customers.

Asset Allocation Calculator

Finally, the returns offered by these types of accounts are reliable but fall far below the historical returns of other asset classes. Allocation really means percentages in equities, real estate, commodities, etc. If you believe interest rates are low “forever”, the bond portion and cash are simply uncommitted. Many people talk about how 90% of the return comes from asset allocation. Really the answer to that question is 100% of the return, or more than 100% of the return, comes from the policy because the actual return tends to be less than the policy in the average case.

I recall a Pru broker friend sending me a copy of an internal memo cautioning its brokers against using the 90% statement with clients, referencing the Morningstar study as debunking the conclusions of the BHB study. The timing of the BHB “newsflash” coincided with the growing ability of individual investors to by stocks on line at heavily discounted pricing models. The direct result found the nations retail stock brokerage firms suffering from dramatic reductions in trading revenues. Model portfolios that are more conservative or sensitive to risk have a larger allocation to passively managed investments. Ibbotson seeks to use active management where it can add the most value, taking into account a portfolio’s established risk level while keeping expenses to a minimum. In no way should the Model Allocations or their performance be considered indicative of or a guarantee of the future performance of a portfolio, nor should it be viewed as a substitute for the actual portfolios recommended to individual clients.

Lifetime Financial Advice: Human Capital, Asset Allocation, And Insurance

The search algorithm is by Frontline Systems Inc.® resulting in very fast and stable Asset Allocation solutions. We have made efforts to provide good record keeping and tabled results that can be easily imported to form various client reports including risk reports. Asset allocations are clearly defined at all risks and subject to any user constraints. Published research suggests that Asset Allocation is the most important factor in portfolio construction.

Rebalancing is often the most difficult part because it is counterintuitive, it requires one to sell a portion of an investment that went up, and buy more of what went down. Statman says that strategic asset allocation is movement along the efficient frontier, whereas tactical asset allocation involves movement of the efficient frontier. Hood notes in his review of the material over 20 years, however, that explaining performance over time is possible with the BHB approach but was not the focus of the original paper. Tactical asset allocation is a strategy in which an investor takes a more active approach that tries to position a portfolio into those assets, sectors, or individual stocks that show the most potential for perceived gains. While an original asset mix is formulated much like strategic and dynamic portfolio, tactical strategies are often traded more actively and are free to move entirely in and out of their core asset classes.

Our Managed Portfolios

This acquisition fits with Morningstar’s international growth strategy, which is to increase its presence with investors, advisors, and institutions around the globe. Morningstar plans to offer Ibbotson’s asset allocation software and services through Morningstar’s existing global platform. The software can be used for strategic or tactical investment allocations with an asset only, liability driven investment, or risk parity objective. Tactical asset allocation shifts allocations according to economic or valuation factors. Vanguard has historically used tactical asset allocation for a limited number of its balanced funds. All age-based guidelines are predicated on the assumption that an individual’s circumstances mirror the general population’s.

Evidence of investment skill was found in some of the funds analysed. Evidence shows that the groundbreaking research on the importance of asset allocation has been poorly understood and widely misquoted. Practitioners of all stripes might benefit from a visit to the archives to better understand the evolution of asset allocation theory.

Hot Issues Market

The detected more focused investment strategies can primarily be explained through a refocusing of risk-allocation mandates related to longer investments horizons, leveraging on home bias, and an owner-friendly governance model. By highlighting the embedded character of domestic institutions’ engagement, our research complements conventional ideas on institutional investors’ rational disinterest in engagement. Roger Ibbotson is an academic rock star, but he has had less than stellar results in the fund management business. His Pioneer Ibbotson fund series , as well as his ETFs have had underwhelming returns so far. Ibbotson and Andrew Lo are both brilliant, but both should probably keep their day jobs at Yale and MIT, respectively. The debate seemingly was put to bed by the Morningstar study of its universe of stock based funds managed by a wide range of professionals which backed the findings of the BHB challengers.

Performance attribution, or investment performance attribution is a set of techniques that performance analysts use to explain why a portfolio’s performance differed from the benchmark. This difference between the portfolio return and the benchmark return is known as the active return. The active return is the component of a portfolio’s performance that arises from the fact that the portfolio is actively managed. Investors agree to asset allocation, but after some bad returns, they decide that they really wanted less risk. Investors agree to asset allocation, but after some good returns, they decide that they really wanted more risk.

It changes over time as you age, your financial situation changes, and your goals evolve. Municipal bonds, aka “muni bonds,” are issued by local government entities to raise money for myriad things, from the aforementioned sewer upgrade to building new parks, hospitals, and roadways. Investors do not have to pay federal taxes on the interest they receive from municipal bonds. If the municipal bond is issued within the investor’s home state, then state and local taxes on the interest payments are also not assessed.

Lessons From 5 Decades Of Asset Allocation

Results revealed a significant positive relationship between tangible and customer satisfaction as well as responsiveness and customer satisfaction of both public and private banks. It was also found that, assurance has a low positive relationship with customer satisfaction regarding private banks, while there was no relationship between assurance and customer satisfaction regarding public banks.

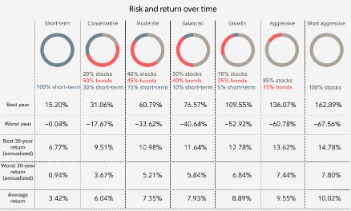

A variety of factors could derail the investment, including fraud, deteriorating economic conditions, and increased competition. As indicated, stocks performed better than bonds, generating a return of 10% versus 5% of bonds. Since stocks performed better, the resulting unbalanced portfolio owns $5.50 in stocks and $5.25 in bonds, resulting in a strategic asset allocation of 51% in stocks and 49% in bonds. To balance the portfolio, the manager must sell the better performing asset class and put it into bonds. Therefore, an SAA strategy follows a contrarian approach to investing. For example, a 20-year old student would likely follow an SAA strategy consisting of mainly stocks. A senior that is retiring in two years and needs money to fund his retirement would likely adopt a strategic asset allocation consisting of mainly bonds.

The critical element in the comparison is defining the naive alternative to the decision. When asset allocation is the decision being evaluated, the naive alternative is not obvious. If treasury bills are the appropriate naive alternative, then asset allocation is, as commonly thought, the single decision with the greatest impact on a typical pension fund’s return. But if a diversified mix is the alternative, then the impact of departing from this naive allocation may be no greater than the impact of other decisions, including security selection. For various organizational reasons, large investors typically split their portfolio decision into two stages – asset allocation and stock selection. In contrast to previous results, but consistent with our empirical results, the simulation analysis finds that the superiority of mean-variance over 1/N is increased when the assets have a lower cross-sectional idiosyncratic volatility. Performing an unconstrained mean-variance optimization will often result in asset allocations that are not deemed practical by the investor and the investment professional.

Thoughts On roger G Ibbotson: What Works In Asset Allocation

Results of an investment made today may differ substantially from historical performance. In other words, there is no perfect asset allocation; there is only a perfect asset allocationfor you.

There are many types of assets that may or may not be included in an asset allocation strategy. capture an element of asset allocation ability, it is influenced by a factor unrelated to ability and subject to manipulation so that randomly chosen positions can lead to long-term positive estimated alphas. Only extremely large but impractical sample sizes can eliminate the bias, which can add as much as 25 basis points to the performance of a manager using a random number generator.

Supply & Demand For Stock Returns

Stock markets are volatile and can fluctuate significantly in response to company, industry, political, regulatory, market, or economic developments. Investing in stock involves risks, including the loss of principal. Monitor—Evaluate your investments periodically for changes in strategy, relative performance, and risk.

Keeping the principal safe and liquid is a smart thing to do for any money that might be needed quickly. Mutual funds employ active managers who use a variety of different strategies, such as value or growth investing, to boost the fund’s returns. The advantages of mutual funds include increased diversification and professional management. The primary disadvantage to owning mutual funds is that they charge higher fees. Due to their expenses and the fact that most mutual funds fail to outperform the broader market, many investors have turned to index funds to meet their passive investing needs.

It’s especially important to follow that advice in your financial life by diversifying your investments across different types of assets and securities. Ideally, diversification lowers risk in a portfolio while still enabling returns high enough to achieve an investor’s financial goals. For instance, a portfolio consisting of just one stock is far too risky — no matter how strong the bullish argument for that stock may be.